Hi guys, Amit Sharma here. Welcome back to another honest finance reality check.

If you own a smartphone in India today, I can guarantee that you receive at least two text messages or WhatsApp notifications every week that look something like this: “Congratulations! You have a pre-approved loan of ₹50,000. No paperwork, No CIBIL check. Click here to get money in 2 minutes!”

Living and working in टोंक (Tonk), Rajasthan, I interact with a lot of young students, small shop owners, and early-career professionals. Whenever there is a medical emergency, a sudden wedding expense, or even just an urge to buy the latest 5G smartphone, people get tempted by these 5-minute loan apps. They think, “It’s just a small amount, I will pay it back next month.”

But after three years of deeply analyzing the personal finance sector, let me tell you the brutal truth: These instant loan apps are modern-day debt traps.

Today, I am going to pull back the curtain and show you exactly how these apps operate, how they legally loot your hard-earned money, and why hitting that “Apply Now” button might be the worst financial mistake of your life.

The Illusion of Convenience

Why do people love instant loan apps? Because traditional banks are strict. If you go to a regular bank for a personal loan, they will ask for your salary slips, check your CIBIL score, verify your address, and make you sign a mountain of physical paperwork.

Instant apps, on the other hand, just ask you to download their application, upload a selfie, punch in your Aadhaar number, and give them “Permissions” on your phone. Within exactly 5 minutes, the money hits your bank account. It feels like magic.

But as we all know, whenever something looks too good to be true in the finance world, you are usually the product being played.

The Nightmare of “Processing Fees” and Hidden APR

Let’s talk math. When you take a loan from a traditional bank, the interest rate is usually between 10% to 15% per year.

Instant loan apps aggressively advertise that they only charge

“1% or 2% interest.” What they cleverly hide in the fine print is that this is 1% to 2% per month, sometimes even per day! When you calculate the Annual Percentage Rate (APR), these apps are legally charging you anywhere between 36% to an insane 60% per year.

Let’s look at a real-life example: Suppose you borrow ₹10,000 for an emergency from a fast-cash app for a period of 3 months.

-

Loan Amount: ₹10,000

-

Processing Fee Deducted Upfront: ₹1,500 (You only receive ₹8,500 in your bank!)

-

Interest Charged: ₹1,000

-

Total Repayment: ₹11,000

You borrowed ₹10,000, but you practically only got to use ₹8,500. Yet, you are paying back ₹11,000. When you calculate the real math, you are paying over 50% interest!

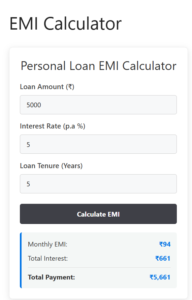

🛑 Don’t Get Fooled by the App’s Math: Before you accept any instant loan, take the actual numbers they are showing you and put them into my free [Personal Loan EMI Calculator] here on the blog. When you see the actual interest breakdown in front of your eyes, you will immediately delete that app.

The “Contact List” Blackmail

What happens if you miss your EMI payment by just one or two days?

With a traditional bank, you get a polite reminder message or a late fee charge. But instant loan apps do not play by the standard rules. Remember those “Permissions” you granted when you installed the app? You gave them full access to your phone’s gallery and your entire contact list.

Many unauthorized Chinese-backed loan apps use a psychological torture method called “Contact Shaming.” If you default, they will create a WhatsApp group with your parents, your boss, and your friends. They will send messages calling you a fraud and a thief. The mental harassment is so severe that many young people in India have unfortunately taken extreme steps due to the public humiliation.

My strict advice: Never install a financial app that asks for permission to read your contacts or view your personal photo gallery. A genuine RBI-registered NBFC does not need to see your family photos to give you a loan.

The Silent Killer: BNPL (Buy Now, Pay Later)

Wait, what if you don’t use shady loan apps? What if you only use the “Buy Now, Pay Later” (BNPL) feature on famous food delivery or shopping apps to order a ₹500 pizza? That’s safe, right?

Wrong.

BNPL is nothing but a micro-personal loan wearing a fancy t-shirt. Every single time you use a BNPL service to pay for a cab ride or a t-shirt, a new “Consumer Loan” is opened in your PAN Card history.

If you forget to pay that ₹500 BNPL bill on time, the company will report you to the credit bureaus. I have seen young college graduates whose CIBIL scores have crashed from an excellent 780 to a terrible 610 just because they forgot to pay a ₹300 Swiggy or Zomato BNPL bill. When they actually need a genuine home loan or education loan 5 years later, regular banks reject them instantly because their credit report is ruined by these micro-loans.

The Real Solution: Build Your Own Bank

The only reason people fall into these high-interest debt traps is because they do not have a backup plan. When an emergency strikes—a hospital visit, a broken laptop, or a bike repair—they panic and download an app.

The ultimate solution to avoid this trap is to build an Emergency Fund.

Start paying yourself before you pay any app. As soon as you get your salary or business income, take 10% of it and lock it away.

🚀 Build Your Wealth, Not Your Debt: Instead of paying 40% interest to an app, what if you earned 12% to 15% interest on your own money? Use my SIP Calculator to see how investing just ₹2,000 every month can build a massive safety net for your future. When you have your own cash reserve, you become your own bank!

Amit’s Final Verdict

The world of instant loans and BNPL looks very attractive from the outside. It is designed to trigger your dopamine and make you spend money you do not actually have.

If you are currently trapped in a cycle of instant app loans, stop borrowing new money to pay off the old ones. Use the Debt Avalanche method (which we discussed in my previous article) to clear the highest interest loan first. Delete the apps, protect your data, and guard your CIBIL score with your life.

Financial freedom doesn’t come from borrowing easily; it comes from saving consistently. Stay smart, stay safe, and keep your hard-earned money in your own pocket!

Amit Sharma is a financial content expert with over 3 years of experience in the banking and lending sector. He specializes in simplifying personal loan eligibility, credit scores, and surrogate loan processes for everyday Indians.